The Impact of Global Tax Reforms on Emerging Economies

Global tax reform has moved from theory to action. The OECD’s BEPS 2.0 framework, especially its Global Minimum Tax (Pillar Two), is already reshaping how multinational companies’ profits are taxed across jurisdictions. For emerging economies, these reforms present both opportunities and constraints: more equitable tax receipts on one hand, and reduced flexibility for tax competition on the other.

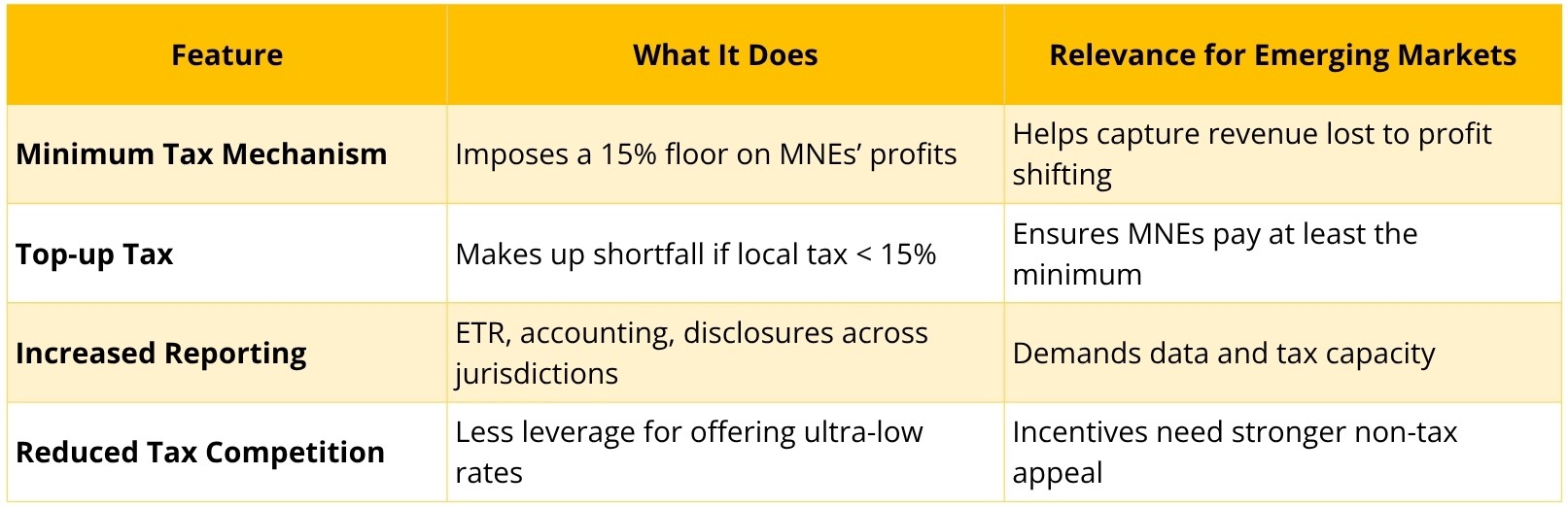

Under the proposed rules, multinational enterprises (MNEs) with consolidated revenues above EUR 750 million will be subject to a 15% minimum effective tax rate, regardless of where they operate. If a country’s domestic tax is lower, the remaining “top-up” tax may be imposed so the effective rate reaches 15%.

Recent estimates suggest that implementing a global minimum tax could raise US$155–192 billion annually in additional corporate income tax revenues globally, representing about 6.5% to 8% of current global CIT collections.

Emerging nations have long struggled with base erosion and profit shifting (BEPS) as multinationals route profits to low-tax jurisdictions. Under Pillar Two, these practices become less profitable. The reform may rebalance revenue flows toward countries where real economic activity occurs.

What This Means for Emerging Economies

Revenue Gains and Trade-offs

Emerging markets stand to benefit from reduced profit shifting, potentially improving their corporate tax receipts. But those gains depend heavily on administrative capacity, legal updates, and cross-border cooperation.

At the same time, countries will lose some of their ability to compete purely on low corporate rates. That means governments must lean more on structural incentives, like infrastructure, skilled labour, and special economic zones, to attract investment.

Implementation Costs and Capacity Challenges

Instituting Pillar Two is not plug-and-play. Countries must build systems for jurisdictional effective tax rate (ETR) calculations, top-up tax collection, dispute resolution mechanisms, and reporting requirements. Those with weak tax institutions may struggle.

Level Playing Field vs. Revenue Redistribution

While reform aims to level the field, the transition phase can favour jurisdictions well ahead in reform implementation and governance. Countries with less negotiation flexibility risk being sidelined.

Below is a compact comparison for emerging markets:

India’s Position and Adjustments

India has already taken steps consistent with the new global tax order. The country already imposes an equalisation levy on certain digital services and is expected to align its corporate tax regime to integrate with global minimum tax rules.

India also continues to deploy targeted incentives, such as in the manufacturing and export sectors, structured within the permissible bounds of international tax norms. This means foreign investors entering India will find a more predictable, rule-based tax environment where alignment with global norms matters as much as headline rates.

What Market Entry and Policy Teams Should Watch

✔ Strengthen enforcement capacity: Advanced audit data systems and automatic exchange of information will be critical.

✔ Rethink incentive models: Moving from rate wars to value propositions—skills, infrastructure, cluster advantages.

✔ Reconfigure multinational structures: Global groups must recast their transfer pricing, funding, and treasury flows to avoid surprise top-ups.

✔ Coordinate tax policy regionally: Harmonised frameworks across neighbouring economies reduce distortion and arbitrage.

Global tax reform is shifting the ground under international investment. For emerging economies, the promise is fairer tax capture; the risk is that weaker systems may get left behind. The competitive edge will no longer be how low a jurisdiction’s tax rate is, but how clearly and consistently it enforces rules.

For firms entering markets like India, the lesson is clear: success will depend not just on business models or product fit, but on mastering global compliance, structuring for evolving rules, and partnering with advisors who understand the new tax terrain.